The Wall Street Journal reported on the 27th that since the outbreak, millions of tenants in the United States have defaulted on rent. As the ban on eviction expires, they may be in danger of being evicted from their homes. Falling into the struggling rental market may trigger the next housing crisis.

The phenomenon of rent arrears has worsened

A study of the unemployed by the Philadelphia Federal Reserve Bank released last week showed that unpaid housing rents will reach $7.2 billion by the end of the year.

Moody’s Analytics estimates that if there is no additional financial relief plan, by the end of the year, the outstanding rent will reach nearly $70 billion.

By then, 12.8 million Americans will default on rent, with an average of $5,400 in arrears. In 2008, the subprime mortgage crisis caused the mortgage houses of 3.8 million residents to be repossessed by banks.

Many analysts warned that the scale of homelessness caused by rent arrears this time may far exceed the previous crisis. The federal government estimates that once the ban on expulsion is lifted, 30-40 million people are in danger of being evicted from their homes.

A survey by the U.S. Census Bureau shows that about a quarter of renters with children are now in arrears with rent, and the proportion of minorities in debt is even higher (above).

The University of California survey found that in pandemic, African Americans and Latinos are twice as likely to be unable to pay rent as whites.

Some people are struggling for next month’s rent, while others are catching up with the real estate express. Because mortgage interest rates are at a historically low level, some mid-to-high-end people who have not been significantly affected by the Pandemic have bought homes.

The confidence index of home builders hit a record high in October, and the sales of second-hand homes in September reached the highest level in 14 years.

It is foreseeable that after the baptism of this crisis, the gap between the rich and the poor between those with and without houses, as well as the housing inequality will further intensify.

Housing inequality exists for a long time

Before the Pandemic, the housing problem in the United States was the most serious among developed countries. According to statistics from the U.S. government in 2019, more than 500,000 people are homeless across the country, and nearly 200,000 people sleep on the streets every day. Like medical care, housing inequality is a chronic disease in American society.

The first is the lack of housing security for low-income families. In the United States today, more than 40 million households rent houses, the number is close to the highest level after World War II, with 17% of households renting more than half of their income. For most families, rent is the biggest daily expense, and the pressure on low-income groups is greater.

However, no state in the United States can provide enough affordable homes for low-income people . Nationwide, there is a shortage of nearly 7 million units of “low-rent housing” (according to the National Housing Alliance for Low-income People).

Housing pressure falls more on ethnic minorities. The U.S. Census Bureau’s report for the first quarter of 2020 shows that black households have the lowest home ownership rate at 44%, which is nearly 30% lower than that of white households.

The price of buying houses for black families is also at the bottom of all ethnic groups.

Blacks usually pay higher interest rates to buy a house with loans, and the probability of rejection is higher. According to data from the National Association of Realtors, more than 13% of black households who applied for a home mortgage were rejected last year, compared with 5% of whites.

In fact, an important manifestation of the racial polarization of the rich and the poor in the United States is the polarization of housing. According to a report by the Urban Institute, if housing equality is achieved, the racial gap between rich and poor will be reduced.

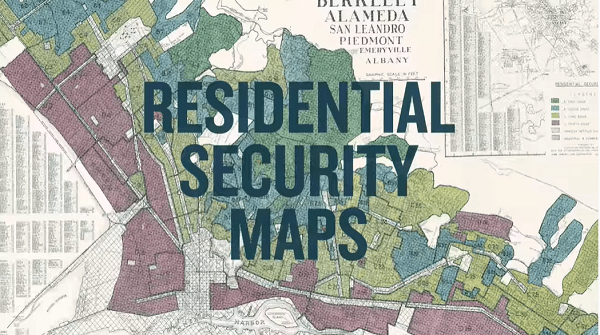

On the other hand, housing inequality also comes from invisible housing isolation. During the Great Depression in the 1930s, US President Roosevelt launched the “New Deal” in an attempt to restart the economy, of which expansion of new housing was an important part.

The Federal Housing Administration (FHA) and the Homeowner’s Loan Company (HOLC) have been established to provide mortgage loans and guarantees for ordinary families.

The homeowner’s loan company created the “House Safety Map” (above), where green is the “best” area, corresponding to the merchant class, blue means “good”, facing white-collar workers, yellow means “salary class”, red It means “harmful area”, which corresponds to the lower-class people, especially black people.

The Federal Housing Administration has also promoted residential segregation, defining black areas as “risk areas” and refusing to provide government mortgage guarantees to black buyers.

Similar stark housing discrimination continued until after the passage of the Fair Housing Act in 1965. Nowadays, although open discrimination is rare, due to factors such as historical evolution, culture, and markets, the “rich areas” and “poor areas” of most American metropolitan areas are still clearly demarcated.

Solve the housing problem and find the middle way

Since the 1930s, the US government tried to solve the housing problem of low-income groups by building public housing, but the effect was not satisfactory.

The concentrated public housing built in the last century has gradually become synonymous with slums. Drugs are rampant, social problems are concentrated, and living conditions are poor.

US federal government gradually withdrew from direct development and operation of public housing, and instead encouraged private enterprises to construct and develop through subsidies and tax cuts.

However, practice has proved that it is not reliable to solve public rental housing completely through a free market economy. For example, the federal government has provided tax credits to private developers through the Low-Income Residential Tax Rebate Policy (LIHTC).

In less than two decades, public costs have increased by 66%, but the number of newly built houses has decreased; the government also provides ” “Housing option vouchers” directly subsidize private landlords, but they are also a drop in salaries.

According to the report of the National Housing Alliance for Low-Incomers, the median waiting time to apply for such a subsidy is 1.5 years, and some people have queued for up to 7 years.

As the Pandemic has led the United States into an economic recession, housing problems have become increasingly prominent, and calls for systematic reforms of federal housing policies have become increasingly loud.

Many reform activists believe that the privatized housing market cannot meet the needs of the people and demand that the housing market be “socialized”; some activists ask the government to curb soaring rents and regulate them; some others suggest that large companies should be taxed , Used to build public housing to solve the problem of short supply.

However, these assumptions run counter to the right-wing thinking that advocates a free market economy, and they will inevitably be labelled “ultra-left”.

In the current situation in the United States where the left and right ideologies are highly opposed and the two parties are politically polarized, it is difficult to be optimistic to find a middle way to fundamentally solve the problem of housing equality.