Economic recovery expectations and OPEC production restrictions have reversed the supply and demand situation, and investor sentiment is similar to the historical high 13 years ago.

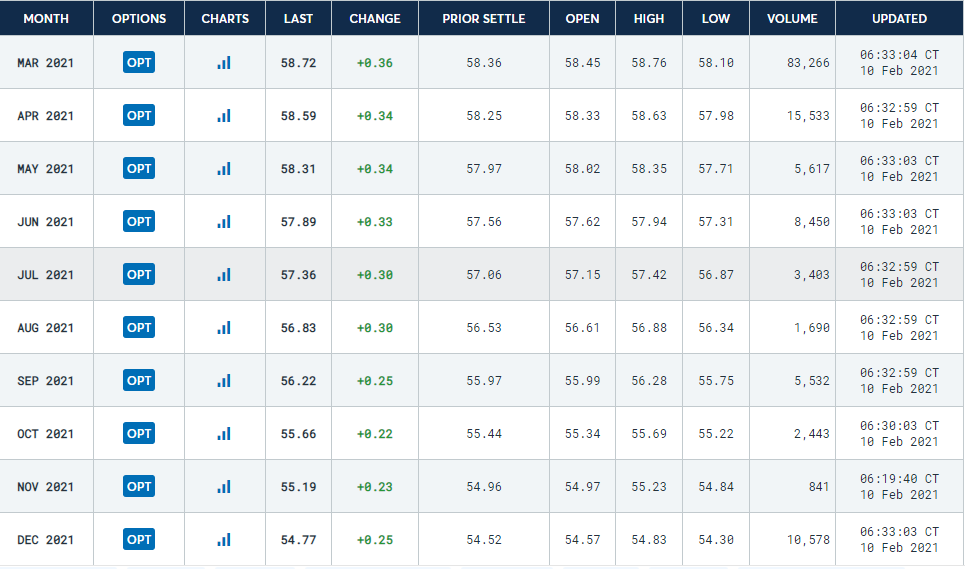

International oil prices have ushered in a dreamy start this year. WTI crude oil and Brent crude oil have hit their highs since January last year, among which Brent crude oil successfully broke through the key psychological threshold of $60.

According to FactSet, a financial information provider, the main contract of WTI crude oil rose 23.1% in the first six weeks of this year, and the main contract of Brent crude oil rose 21.1%.

Market confidence comes from a number of factors: the economic prospects brought about by vaccine distribution, OPEC+ supply restrictions and inventory decline, and the imminent implementation of a new round of U.S. stimulus package, which strengthen investors’ judgment on the reversal of crude oil supply and demand this year.

According to the latest assessment of the Organization of Petroleum Exporting Countries (OPEC), global oil inventories are converging to the five-year average and may fall below this key threshold by the middle of the year.

Tamas Varga, a senior market analyst at PVM Oil Associates, a crude oil broker, said in an interview with First Financial Reporter that the last time the market was so optimistic about oil prices may have been in 2008, when oil prices had risen to $140/ Above the barrel. Now many people have seen a good scene of economic recovery in the next few months.

He expects that oil deployment has the potential to hit $70 in the short term, depending on the effect of epidemic prevention and control, but the rise in oil prices may trigger the motivation of oil-producing countries to revise production reduction agreements, putting pressure on the relationship between supply and demand.

The effect of production control after “Yunman Jinshan” appears.

Last spring, because oil-producing countries did not respond in time to the sharp decline in demand caused by the epidemic, global energy inventories were “oily”.

U.S. Cushing crude oil inventory once increased to more than 70 million barrels, accounting for 83% of the working storage capacity.

Market concerns about inventory directly led to the unprecedented “negative oil price” of WTI crude oil in April contract the day before delivery.

Now the situation has improved significantly.

The First Financial Reporter noticed that last week’s U.S. Energy Information Administration EIA data showed that the U.S. Cushing crude oil inventory has dropped to a seven-month low of 48 million barrels.

Globally, the large amount of oil reserves accumulated during the epidemic are also decreasing faster than expected.

At present, demand in China and India has recovered rapidly.

The agency predicts that if demand in developed economies picks up, it may pave the way for further energy prices.

The decline in inventory is largely due to the efforts of OPEC led by Saudi Arabia and Russia and its allies to curb production.

OPEC said that since the production cut last April, oil-producing countries have cut production by 2.1 billion barrels.

At the regular meeting of the OPEC Ministerial Oversight Committee held in early February 2021, countries strengthened the consensus on production restrictions, hoping to “accelerating market rebalancing” and emphasizing their optimism about the long-term recovery in 2021.

Export data released by OPIS/IHS Markit for January showed that maritime oil flows from member countries decreased by 900,000 barrels per day to 23.3 million barrels per day, and the decline in inventories in February and March may accelerate due to an additional voluntary production reduction of 1 million barrels per day by Saudi Arabia.

Varga told the First Financial Reporter that with the launch of vaccine distribution procedures in various countries, the number of vaccinated people worldwide has now exceeded the number of confirmed cases, which brings hope for epidemic control and economic recovery, and commodities, including crude oil, have begun a new round of rise.

The current bull market may only be destroyed by disputes among OPEC members or virus mutations beyond control.

The derivatives market reflects investors’ enthusiastic expectations.

Brent crude oil bulls surged 23% to 66 million barrels and reached $19 billion in contract value in the five weeks ended February 2, compared with $14 billion by the end of 2020.

During the same period, the bullish bet on WTI crude oil on the Chicago Mercantile Exchange also increased to 19 million barrels.

At the same time, the discount between crude oil futures contracts has further expanded, indicating that the market expects that the risk of crude oil shortage will rise in the short term.

At present, the December contract of WTI crude oil in the United States is nearly $4 per barrel compared with the March contract, the widest level since March last year.

The United States and OPEC are still variables.

As in the past decade, the future trend of oil prices is still affected by the production trend of major oil-producing countries such as OPEC and the United States.

U.S. crude oil production has not yet fully recovered. According to the data of the U.S. Energy Information Administration (EIA), domestic crude oil production in the United States is currently 11 million barrels per day, down 17% from the peak.

It is worth noting that the volume of active crude oil drilling rigs in the United States has recently begun to rise.

According to oilsuit giant Baker Hughes, the number of drilling rigs has increased from a five-year low of 172 six months ago to 306 last week. Shale oil production rose to 7.61 million barrels per day from a low of 6.75 million barrels per day in May last year.

There are practical difficulties in recovering shale oil production in the short term.

On the one hand, the vitality of energy enterprises has been greatly damaged under the epidemic.

According to the data of Bank of America, nearly $79 billion in high-yield bonds defaulted in 2020, and the energy industry is a “hardest hit area”.

The credit ratings of many exploration companies, including Western Oil, have been downgraded from investment level to speculative rating, that is, “garbage level”.

At present Oil prices do not seem to be enough to support high-cost mining activities.

On the other hand, U.S. President Biden’s clean energy plan will suppress the traditional energy industry.

First Financial Reporter noted that Biden has signed a number of executive orders related to exploration and exploitation of traditional energy industries since taking office, including suspending the construction of the long-disputed Keystone-XL pipeline and suspending new oil and gas drilling on federal land for 60 days, which will prevent the United States.

The federal government’s sale of new mining and mining rights of about 700 million acres is the first important measure to limit the growth of production and supply in the United States in the coming years.

“It is unrealistic to recover shale oil completely in the short term, and that even though technological advances and streamlined structure could make production costs less than $40 per barrel, the breakeven price is unlikely to be the standard for restarting production,” Varga told First Financial Reporter.

Of course, Biden’s policy goals are far away, and while the transition from fossil fuels to renewable energy has undoubtedly begun, global oil demand may take longer to adapt to the new reality, that is, during the transition, the position of crude oil will remain important in the coming years.” He said.

However, if oil prices rise further, OPEC’s next production plan may also become a risk point.

According to the schedule, OPEC+ oil-producing countries will hold a joint ministerial meeting on March 3 to discuss the next production plan.

Varga believes that OPEC+ production cuts are now essential for market stability, and Libya, Iran and other countries not subject to production cuts are potential threats to the balance between supply and demand.

Judging from the two meetings this year, the oil-producing domestic departments are divided on the production reduction agreement, mainly worried about the loss of market share and the impact of the petrodollar, and many countries are highly dependent on energy finance.

In addition, whether Saudi Arabia’s voluntary production cuts will be postponed after expiration and how quickly the future energy demand will recover are all factors affecting the market’s assessment of supply and demand relationship.” Of course, there is an important premise for all this.

Vaccines can effectively control the spread of the virus, otherwise the market will remain fragile. He said.